The Appraisal Bias Debate: Technology's Role and Its Limitation

I read the CUInsight article, “Can Advances in Valuation Technology Eliminate Appraisal Bias?” (https://www.cuinsight.com/can-advances-in-valuation-technology-eliminate-appraisal-bias/). I understand why the topic draws attention, especially given the seriousness of bias allegations. But the argument that Automated Valuation Models are the solution raises several practical questions that the article never fully addresses.

Here is what does not make sense to me. If millions of appraisals are supposedly so biased or unreliable that we need to shift toward automated models, why are those same appraisals being fed into systems like the Uniform Collateral Data Portal and used to train the very models that are positioned as replacements? Either the underlying data is fundamentally flawed, or it is reliable enough to build on. The logic cannot reasonably support both positions at once.

You cannot describe the data as broken and then rely on it as the foundation for something better.

What AVMs Miss Because I See It Every Day

I walk properties where the MLS says “fully renovated kitchen,” only to find builder-grade cabinets from 2005 with a coat of white paint and little else changed. I measure square footage listed at 2,400 square feet and document an ANSI-compliant figure closer to 2,080. I appraise homes marketed as “waterfront” where the view is actually a drainage canal partially blocked by fencing and overgrown landscaping.

An AVM does not walk through that house or open cabinet doors. It does not notice that the “fourth bedroom” has no closet and functions more like a flex space than a true sleeping area. It reads what is entered into the database and processes it without context.

I deal with incomplete or inconsistent MLS data constantly. That includes inflated GLA figures, overly generous condition descriptions, and vague renovation claims that sound impressive but lack substance. A substantial part of my job involves verifying and correcting that information before I even begin comparative analysis.

When automation analyzes imperfect inputs without field verification, it does not eliminate error. It distributes it at scale.

The Bias Conversation Needs Precision

The article references the 2018 Brookings study reporting a valuation gap in majority-Black neighborhoods. That study sparked an important national conversation and deserved thoughtful analysis. At the same time, the study acknowledged the role of broader economic and historical forces, including long-standing policy decisions and disparities in investment.

As appraisers, we analyze market transactions as they occur. We do not determine zoning, infrastructure investment, lending standards, or school funding. When markets reflect long-standing economic disparities, those realities show up in comparable sales data whether we like it or not. Reporting those conditions is not the same thing as creating them.

I am not suggesting bias has never occurred. It has, and when it does it should be investigated and disciplined. But conflating systemic socioeconomic disparities with the routine work of licensed appraisers oversimplifies a far more complex issue.

When an appraiser crosses ethical or professional lines, there are formal mechanisms for accountability. Those include state boards, USPAP enforcement, and license discipline. Those systems are real and active rather than theoretical.

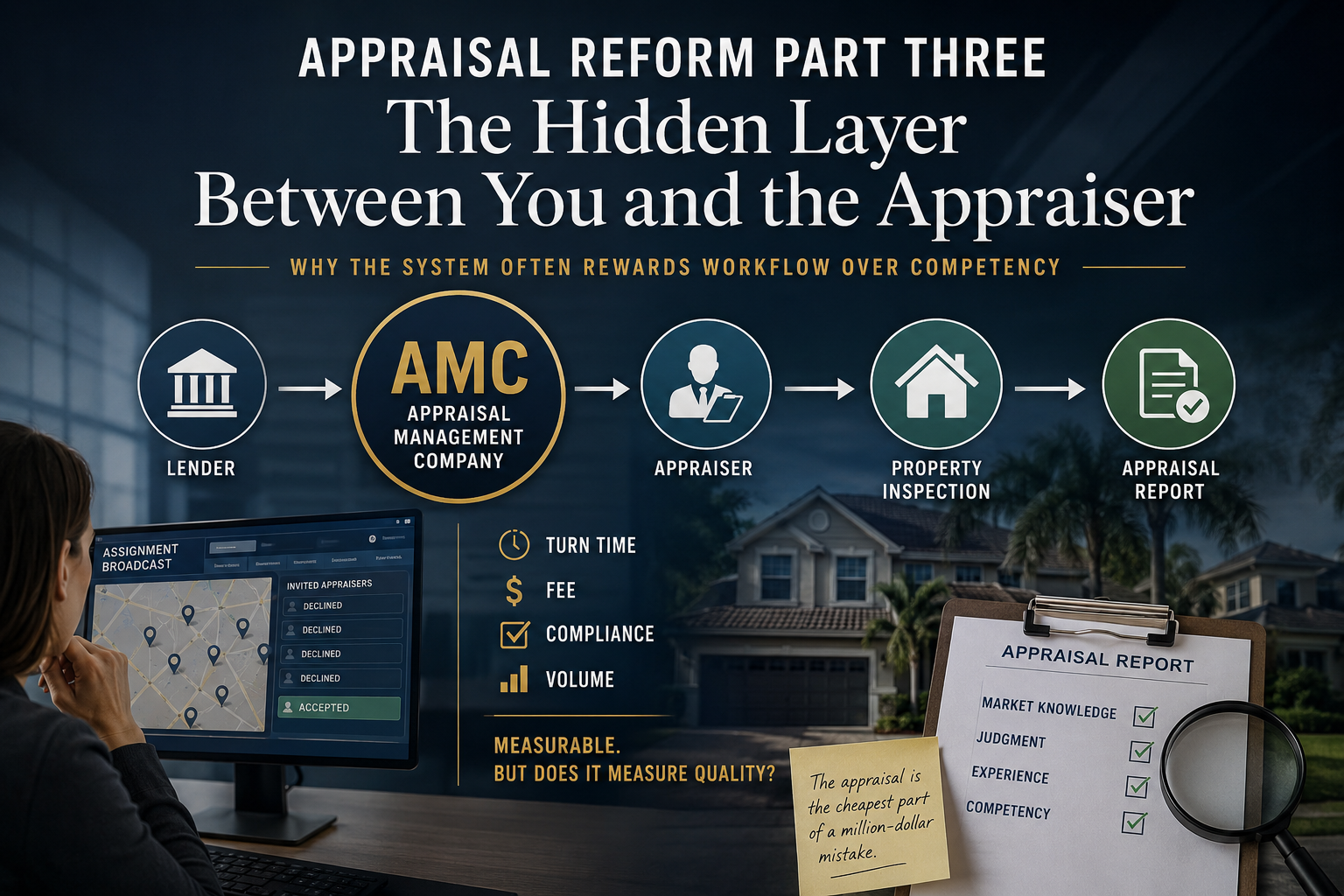

Let’s Talk About Incentives

There is another dimension that rarely gets discussed openly. It involves the incentive structure inside the valuation process itself. Many of the organizations pushing automation are affiliated with Appraisal Management Companies that profit from integrating technology deeper into the pipeline.

In practice, I have seen assignments where the offered fee was so compressed that experienced appraisers declined the work. The file then circulated until someone less seasoned accepted it. That dynamic is not a technology problem. It is an incentive problem.

Consistently selecting professionals primarily on cost rather than competency will affect quality. Replacing experienced field professionals with automated systems does not correct that incentive structure. It simply consolidates control and margin within the intermediary.

Technology absolutely has a place. I rely on data tools every day. But when automation is positioned as a substitute for local expertise rather than a supplement to it, the conversation shifts from improving quality to restructuring who controls the process.

Where Professional Judgment Still Matters

Recently, I appraised two properties in the same waterfront-oriented market. They sat only a few streets apart and appeared similar in size and age on paper. The AVM ranges were tightly clustered.

In reality, one property had unobstructed Gulf access and a functional layout that buyers clearly preferred. The other required navigating a low bridge at high tide and showed deferred maintenance that was not visible in listing photos. Buyers in that market recognized the difference immediately. So did I.

That distinction is not something an algorithm trained on square footage, year built, and zip code alone can reliably capture.

We are not obsolete because we measure variables machines cannot yet interpret consistently. We analyze context, verify data, and apply professional judgment to imperfect information in ways that materially affect outcomes.

A Balanced Approach

Bias should never be dismissed. Concerns about fairness in housing deserve evidence-based discussion. But replacing human appraisers with systems built on the same historical datasets does not eliminate disparity by default.

Improving valuation quality requires raising competency standards and enforcing ethical rules consistently. It also requires aligning compensation with expertise. Technology should enhance independent analysis rather than bypass it.

For property owners and lenders navigating these debates, credibility still rests on verified data interpreted by someone who has physically observed the property and understands how it competes within its specific market. That combination of fieldwork and analysis remains essential in complex or nuanced assignments.

At Gulf Stream Residential Appraisal, I combine on-site inspection, local market knowledge, and rigorous data analysis to produce valuations that reflect how properties actually compete in the real world. If you want to understand how that process works and where technology properly fits into it, you can learn more here:

Hey, I’m Shane. I’m a certified residential appraiser here in Southwest Florida, and I focus on complex valuation assignments and helping people understand real estate value with clarity.