Appraisal Reform, Part One: What the Structural Critique Misses About Real Transactions

On February 17, 2026, Cindy Chance, former CEO of the Appraisal Institute, published a detailed article on LinkedIn titled How Regulation and Calcified Appraisal Education Failed Banks, Consumers, and Real Property Valuation (https://www.linkedin.com/pulse/how-regulation-calcified-appraisal-education-failed-banks-chance-acere/?trackingId=phVkDKI9S5218CcRxVIQsg%3D%3D).

The Appraisal Institute is one of the most recognized professional organizations for real estate appraisers in the United States, and it awards the MAI and SRA designations that reflect advanced education and experience. Chance led that organization and understands how the regulatory and professional structure operates from the inside.

In her article, she argues that the appraisal system has become overly focused on rules and procedures while failing to adapt to changes in lending, data, and market behavior. She points to slow-moving education standards, heavy regulation, the rise of Appraisal Management Companies after Dodd-Frank, and the expanding use of automated valuation systems in mortgage underwriting.

Her article focuses on structure and governance. What it does not fully explore is how those structural decisions affect real buyers and sellers when a transaction is unfolding, and money is about to change hands.

That is where this conversation needs to continue, because for most people, an appraisal is not a policy debate but the number that supports the mortgage on their home.

How the Current System Was Built

After the savings and loan crisis in the 1980s, Congress passed the Financial Institutions Reform, Recovery, and Enforcement Act of 1989, commonly known as FIRREA (https://www.congress.gov/bill/101st-congress/house-bill/1278). That law required lenders to use licensed or certified appraisers for federally related mortgage transactions and required those appraisers to follow uniform professional standards known as USPAP.

Congress authorized The Appraisal Foundation to establish those standards and define minimum qualifications for appraisers, while the Appraisal Subcommittee was created to oversee how states regulate licensed professionals.

The goal was straightforward. Trained, independent appraisers applying consistent standards would provide reliable opinions of market value to support mortgage lending decisions.

For many years, that system brought consistency and accountability to real estate valuation. Over time, however, lending models and securitization practices changed, and the rules did not always keep up with how lending actually works.

That broader concern sits at the center of Chance’s critique.

What Changed After the Financial Crisis

Following the 2008 housing crash, Congress passed the Dodd-Frank Wall Street Reform and Consumer Protection Act (https://www.congress.gov/bill/111th-congress/house-bill/4173), which included provisions designed to strengthen appraisal independence and reduce pressure from loan production staff.

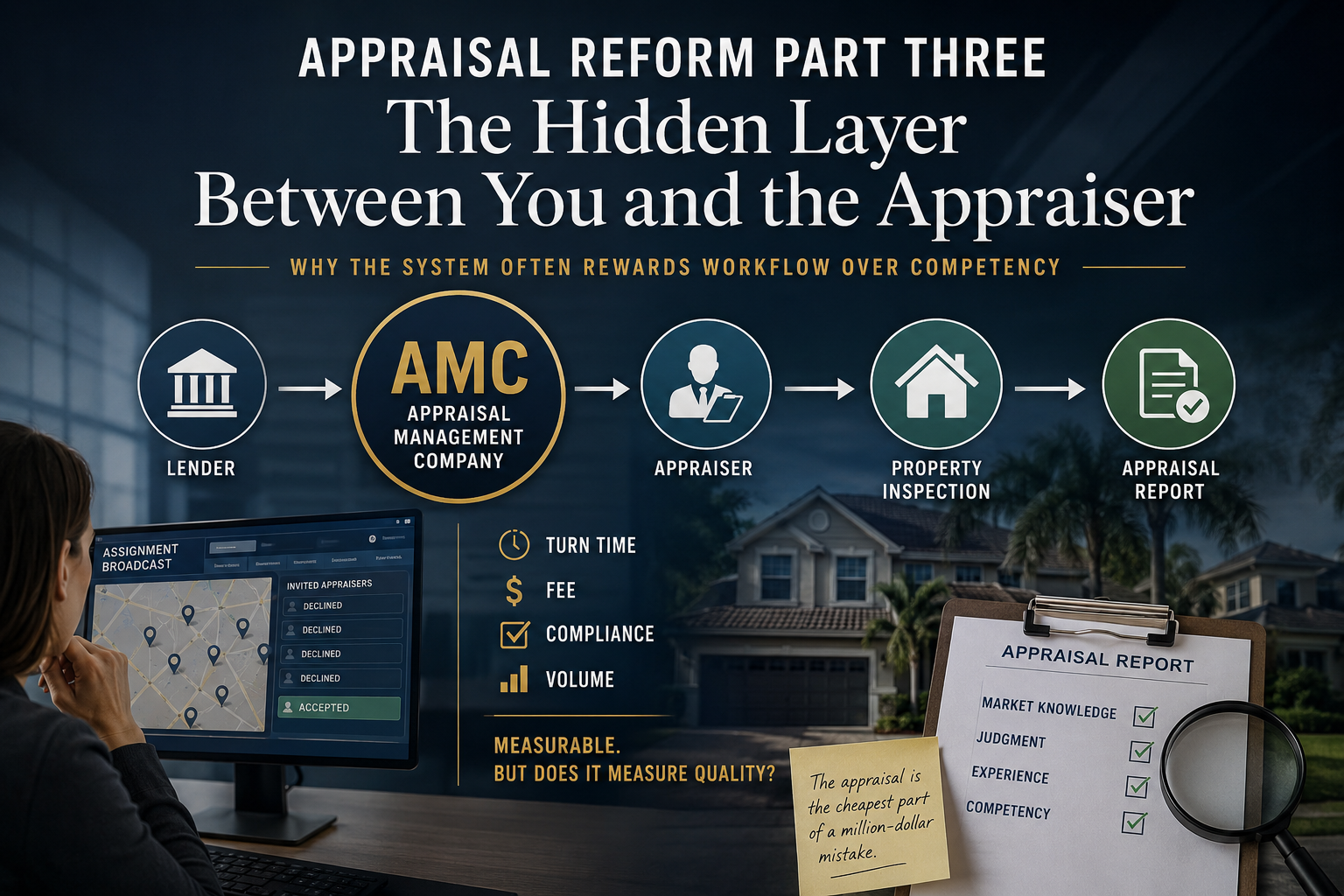

Many lenders responded by relying more heavily on Appraisal Management Companies, often referred to as AMCs, which act as intermediaries between lenders and appraisers. Instead of selecting and communicating directly with appraisers, lenders began routing orders through third-party companies that manage panels, deadlines, and revision requests.

That part made sense. It reduced direct pressure. At the same time, it shifted how performance is measured, because turnaround time and checklist completion are easier to track than depth of analysis or local market knowledge.

When speed and process become the main things measured, they begin to shape behavior. Over time, that shapes which appraisers get work and how much time they spend on it.

The Growth of Appraisal Waivers

In recent years, automated underwriting systems used by the government-sponsored enterprises have expanded the availability of appraisal waivers. When a property and borrower profile meet certain criteria, the system may determine that enough data already exists to support the loan without a traditional appraisal.

These systems review past sales and crunch the numbers. In neighborhoods where homes are similar and sell frequently, that approach, in theory, can work reasonably well.

The problem emerges when a property does not fit neatly into those patterns.

Some homes have not been listed publicly in decades, which means there are no recent interior photographs and no record of what work was done or when. The difference between a fully renovated home and one that has not been meaningfully updated in many years can be substantial, yet public records often do not reflect that difference.

I have been hired to appraise properties in exactly those circumstances. In one case, I was preparing to observe a home where it was unclear whether the improvements still contributed meaningful value or whether the land itself had become the primary driver of pricing. Before I could conduct the site visit, the assignment was canceled because an appraisal waiver had been granted, and no qualified professional evaluated the current interior quality, makeup, and condition.

In another assignment, I was nearly finished analyzing a home in a modest neighborhood that was selling for more than any previous sale in the area, even though the property itself was not especially unique. Before the report was delivered, I was informed that a waiver had been issued and the appraisal would not be used because the loan was cleared to proceed without it.

From a production standpoint, that sequence is efficient and predictable within modern underwriting systems. From a risk standpoint, it raises meaningful questions because a substantial mortgage was approved without someone who walked through the house and knows the market weighing in on how the quality, condition, and features would actually change what a buyer would pay.

If a buyer closes using a waiver and later discovers major deferred maintenance or incorrect gross living area figures, for example, the automated system did not necessarily fail. It simply did not include a qualified analysis of how those conditions influenced market value at the time of closing.

Not every traditional appraisal is better than every automated estimate, and quality matters in both settings. When valuation decisions are driven primarily by speed and cost efficiency, however, important details can be overlooked without anyone deliberately intending that result.

Why This Should Matter to Buyers and Sellers

Most buyers assume the appraisal protects them from overpaying, while most sellers assume it confirms that the contract price reflects current market conditions. Lenders treat it as a key part of collateral risk management within the underwriting process.

When valuation shifts toward automated pathways in situations where property condition and updates actually change what a buyer would pay, borrowers may be taking on more uncertainty than they realize.

Real estate value is not determined by square footage and prior sales data alone. It is also shaped by condition, amenities, and how buyers respond to a property in the current market, which requires someone who has observed the property firsthand, understands valuation theory, and knows the local market.

Cindy Chance’s article explains the structural weaknesses within the appraisal governance system. From inside real transactions, those weaknesses can appear as decisions that move fast and check boxes instead of looking closely, especially when the lender plans to sell the loan and will not be holding the risk long term.

That does not mean the system is beyond repair, nor does it mean that every waiver or automated estimate is inappropriate. It does mean we should be asking whether property values are being determined with the same level of care as the size of the loans they support.

When a property is not fully evaluated in light of its actual quality and condition and how buyers would react to it, the uncertainty does not disappear. It becomes embedded in the mortgage.

Valuation is not simply a step in the mortgage process. It is the foundation that supports the loan.

Shane White is a certified residential appraiser serving Southwest Florida. Learn more about my residential appraisal services here.

Hey, I’m Shane. I’m a certified residential appraiser here in Southwest Florida, and I focus on complex valuation assignments and helping people understand real estate value with clarity.