Appraisal Reform, Part Two: The Incentive Problem No One Talks About

Part One of this series focused on how structural changes in the appraisal system affect real residential transactions, particularly the growing disconnect between procedural efficiency and actually understanding the property securing the loan. The next question is why those changes happened in the first place, and a large part of the answer comes down to incentives.

Most buyers assume the lender making the mortgage will continue carrying the risk tied to that loan for decades, but in many cases, that is no longer how the system works. Today, most conventional residential mortgages are ultimately sold into the secondary market rather than held by the original lender for the life of the loan, largely through structures tied to the government-sponsored enterprises (GSEs) and mortgage-backed securities markets. Research from the Urban Institute regularly tracks the dominant role of GSE-backed and securitized lending within the modern mortgage system (https://www.urban.org/research/publication/housing-finance-glance-monthly-chartbook-september-2025). Once that happens, the lender that originated the mortgage may no longer be carrying the long-term risk tied directly to that specific property.

That changes the relationship between the lender and the underlying asset in ways most borrowers never really see.

If a lender plans to hold a mortgage for thirty years, then the condition, marketability, and long-term stability of the property become critically important because the lender remains directly exposed to the outcome. If the loan is expected to move into a larger mortgage pool shortly after closing, speed and efficiency naturally start carrying more weight in the process.

That difference matters because large financial systems eventually organize themselves around the incentives built into them.

The Quiet Shift From Property Analysis to Process Management

Modern mortgage transactions move fast, and buyers now expect quick approvals, while real estate agents expect tight timelines, and borrowers compare lenders partly based on convenience and how quickly the deal can close.

Inside that environment, underwriting systems increasingly focus on automation, consistency, and workflow management because those things scale efficiently across large loan volumes. That is part of the reason appraisal waivers expanded so aggressively over the last several years. If enough historical data exists, the system may decide that the property risk is already sufficiently understood without requiring a traditional appraisal.

In highly uniform neighborhoods, that logic can work reasonably well because a subdivision filled with nearly identical homes and a strong recent sales history creates predictable data patterns.

The problem is that underwriting systems do not experience uncertainty the way people do.

A local appraiser walking through a property may notice deferred maintenance, poor renovation quality, unusual floorplan changes, micro-location influences, or signs that buyers would react differently to the home than the raw data suggests. Those details can materially affect value even though they may never appear in public records or automated datasets.

The automated system only sees the information that already exists in the data, which means it can only analyze patterns it already recognizes.

In certain transactions, the focus quietly shifts from “understand the property” to “keep the closing on schedule,” and while nobody usually says that directly, everyone involved understands the timeline and pressure surrounding the deal.

Where This Shows Up in Real Transactions

One of the stranger things about residential valuation right now is seeing how differently transactions are treated depending on which underwriting path the loan follows.

There are situations where a lender will waive the appraisal entirely on a property with very limited public information, while another file involving a much more straightforward house may require a full appraisal with multiple rounds of underwriting questions and revisions.

The difference is often not the actual complexity of the property itself. It is the way the system categorizes the risk.

I have seen transactions where a waiver was granted even though nobody involved had current interior knowledge of the property, and I have also seen traditional appraisal assignments where underwriters heavily scrutinized relatively minor adjustment decisions on standard homes because that particular file happened to move through a different underwriting channel.

That inconsistency creates an uncomfortable question sitting underneath much of the modern valuation process.

Is the system always evaluating actual property risk, or is it increasingly evaluating whether enough data exists to keep the process moving smoothly?

Those are not always the same thing.

Why Speed Starts Winning

If the market rewards speed, efficiency, and production volume, then every part of the system gradually adapts around those priorities.

The appraisers who work fastest tend to get more work, lenders that close loans quickly become more competitive, and automated systems reduce friction while shortening timelines.

Careful property analysis is harder to measure than speed.

A strong appraisal is not simply a report that arrives quickly and checks required boxes because a strong appraisal reflects local market knowledge, competent observation, good comparable selection, and an understanding of how buyers actually behave in the current market.

Those qualities are harder to measure on a spreadsheet, which means systems naturally drift toward the things they can easily track.

The Experience Problem Few People Discuss

Another issue that rarely gets discussed outside the profession is experience.

As appraisal fees compressed over time in many lending channels, experienced appraisers began reducing lender work or leaving those assignments altogether, while some AMCs increasingly relied on newer appraisers willing to work at lower fees and faster turn times.

That does not mean newer appraisers are automatically less competent because every experienced appraiser was once new.

The concern is that residential valuation is heavily experience-based, especially in changing or complex markets where understanding how buyers react to a property is not always obvious from raw data alone. Much of that understanding comes from years of seeing transactions succeed, fail, renegotiate, or sit on the market.

That becomes more important as hybrid valuation products expand and parts of the inspection process are increasingly delegated to third-party property data collectors who may have little long-term connection to the profession itself.

As home prices continue climbing, the question becomes whether the system still places enough value on experienced market observation relative to the size of the financial decisions being made.

What Happens When the Market Changes

Many modern valuation systems were developed during periods of strong appreciation and heavy transaction volume, and rising markets can hide weaknesses because increasing prices often cover mistakes.

The real stress test comes when markets flatten or soften because buyers become more selective, and condition differences matter far more than they did in rapidly rising markets.

A house that easily attracted multiple offers during strong appreciation may sit much longer once conditions change, especially if buyers begin paying closer attention to deferred maintenance, floorplan issues, location drawbacks, or renovation quality that stronger markets previously masked.

That is when the difference between historical data and current buyer behavior becomes much more important.

The Bigger Question

The larger issue underneath all of this is whether the modern mortgage system still treats valuation as serious property analysis or whether it is gradually becoming a procedural step designed mainly to keep transactions moving.

If speed, transferability, and production efficiency become the dominant priorities, then every participant in the system gradually adapts around them, including lenders, AMCs, appraisers, and automated systems.

Most borrowers never see that shift happening because the loan still closes and the paperwork still looks complete, but the uncertainty does not disappear simply because the transaction finished successfully. It becomes part of the mortgage itself.

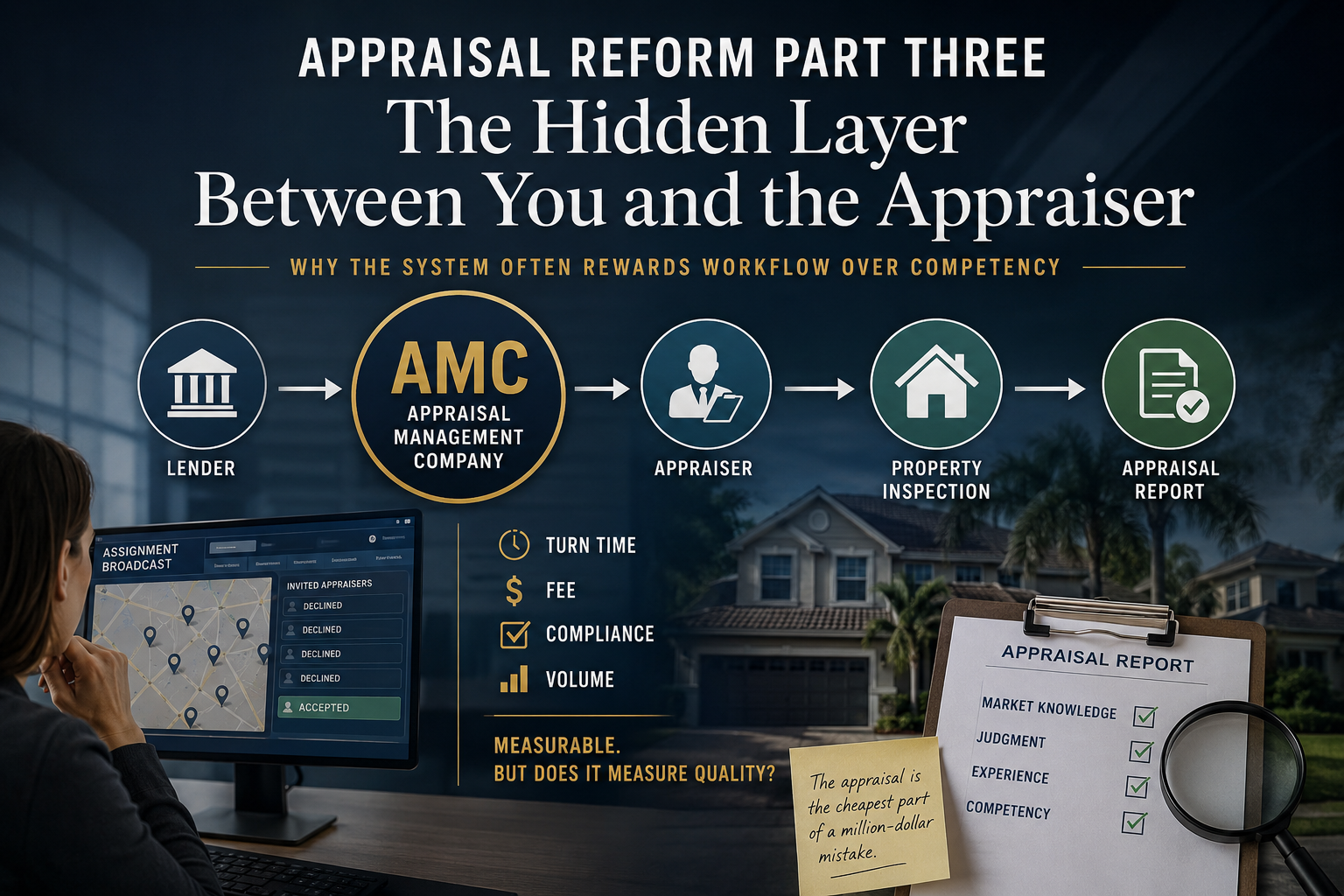

In Part Three of this series, I will examine how Appraisal Management Companies changed the profession itself, including competency concerns, panel selection pressure, and why many experienced appraisers believe the industry increasingly rewards speed over depth.

As more of the mortgage process becomes automated, understanding what a property is actually worth does not become less important. If anything, the stakes become higher.

Hey, I’m Shane. I’m a certified residential appraiser here in Southwest Florida, and I focus on complex valuation assignments and helping people understand real estate value with clarity.