Appraisal Reform Part 3: How AMCs Influence Appraiser Selection and Quality

Appraisal Reform Part Three: The Hidden Layer Between You and the Appraiser

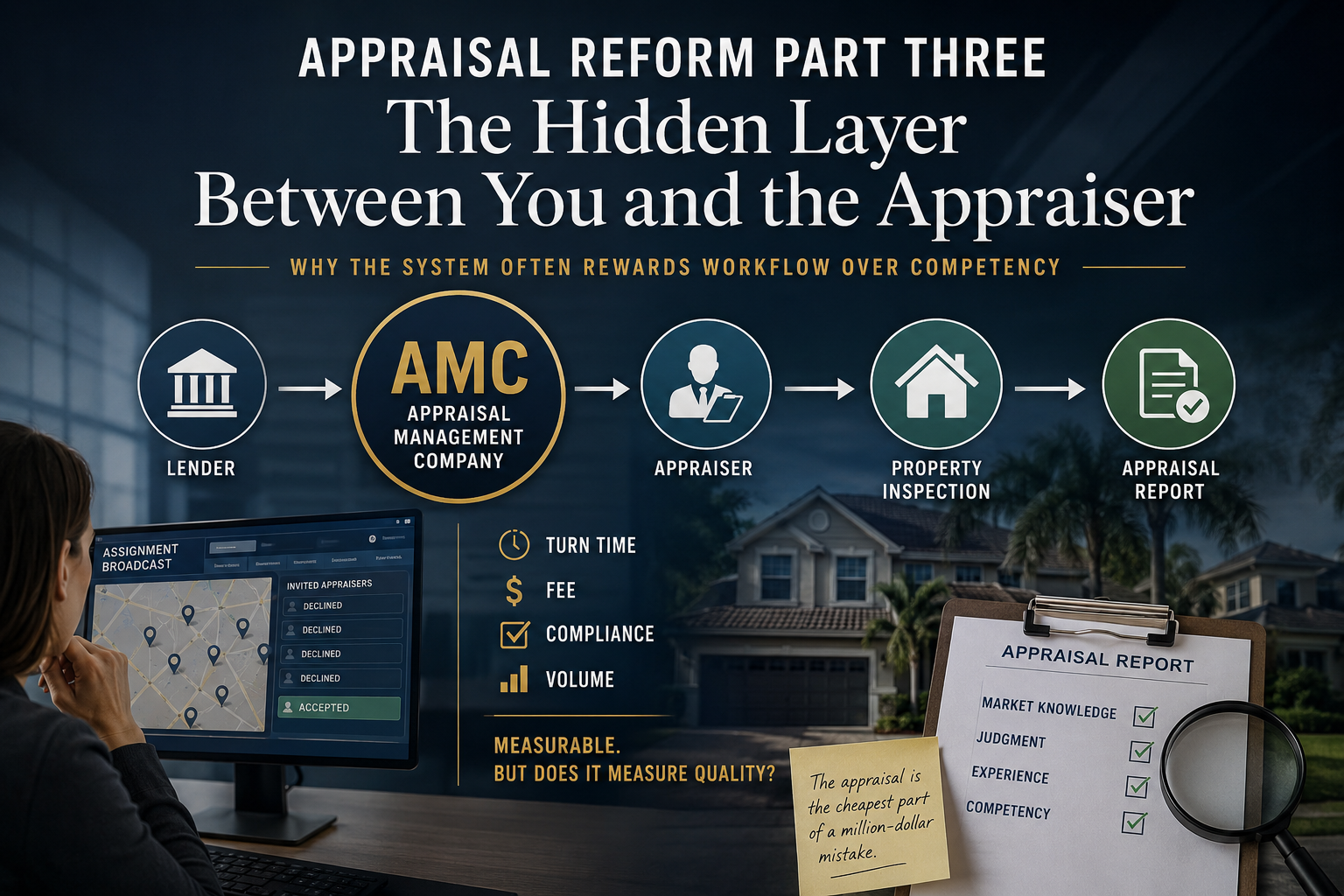

Most consumers think the appraisal process is simple. The lender orders an appraisal, an appraiser inspects the property, and a report comes back. In many mortgage transactions, there is another layer in the middle, and that layer can shape the entire assignment.

If you have not read Part One or Part Two yet, those articles provide the background for this discussion. Part One looked at appraisal waivers and real transactions, while Part Two examined how secondary market lending changes the incentives behind valuation.

Most people think they understand how an appraisal gets ordered.

The lender needs an appraisal. An appraiser gets assigned. The property gets inspected. A report gets delivered. Everyone moves on with the transaction.

That is how most buyers and sellers picture the process because, frankly, that is how it ought to work.

What many people never realize is that there is often another company sitting between the lender and the appraiser making decisions that shape the assignment long before the appraiser ever pulls into the driveway.

That company is an Appraisal Management Company, or AMC.

When Cindy Chance wrote about the structural problems facing the appraisal profession earlier this year, much of the discussion focused on governance, education, regulation, and the direction of the profession. Those issues matter, but they also show up in very practical ways inside everyday mortgage transactions, and that is where this series has focused its attention.

Part One of this series looked at appraisal waivers and why replacing property analysis with automation creates risks most consumers never see. Part Two examined how the secondary mortgage market changed lender incentives and slowly shifted the focus toward moving loans efficiently through a system rather than understanding collateral as deeply as possible. This part is about the layer sitting in the middle because if you want to understand why so many experienced appraisers have become frustrated with residential lending work over the last fifteen years, you have to understand what AMCs changed.

This is not an argument that every AMC is bad.

The concept itself is not the problem.

A company focused on finding the right appraiser, respecting competency, understanding local market expertise, and treating valuation as something more than a compliance exercise can absolutely add value to the process.

The concern is that too much of the industry has drifted toward measuring workflow instead of measuring quality because workflow is easier to track.

Consumers rarely think about competency because they assume it has already been handled for them.

If a licensed appraiser shows up at the property, most people naturally assume that person was selected because they were the best available choice to value that particular property.

I wish I could say that assumption is always correct.

When no comps is treated like no problem

One conversation from years ago has stayed with me because it perfectly illustrates the disconnect.

The assignment involved a luxury high-rise condominium where there were very few comparable sales within the project. The market required expanding into competing developments and carefully pairing differences in views, floor levels, amenities, finishes, and buyer preferences before any meaningful comparison could even begin. There was nothing cookie cutter about the assignment, and the amount of research required was going to be substantially greater than a typical condominium appraisal.

I explained that the fee would need to be higher because of the additional analysis involved.

The response came back almost immediately.

"We don't increase fees because there are no comps."

I still think about that conversation.

The lack of comparable sales is often exactly what makes an appraisal difficult.

Anyone can complete an appraisal when there are ten nearly identical sales across the street and every adjustment is obvious. The real work begins when the market stops cooperating, when buyers are comparing properties that are not identical, and when the appraiser has to interpret market behavior instead of simply reporting it.

That is where experience earns its keep.

Valuation is not bookkeeping.

It is analysis.

Licensing is the floor, not the ceiling

The problem is that analysis does not fit neatly into software metrics.

A computer can track whether an assignment was accepted in thirty minutes or two hours. It can measure how quickly an inspection was scheduled and how long it took to answer a revision request. It can tell management exactly how many reports an appraiser completed last month and whether deadlines were met.

It cannot tell anyone whether that appraiser truly understood the market.

Did they recognize that the value was really in the land and not the house?

Did they understand that a canal with direct Gulf access behaves differently than one with multiple bridges?

Did they recognize a highest and best use issue that changes the entire valuation problem?

Did they understand that buyers shopping one luxury tower would never consider another only a block away because the buildings appeal to completely different buyers?

Those questions do not fit inside a spreadsheet.

They require judgment.

That is where the system starts getting uncomfortable because judgment is difficult to standardize.

Licensing is supposed to establish a minimum level of competency, but somewhere along the way many parts of the industry began treating licensing as though it were the finish line instead of the starting point.

A residential license does not magically make someone qualified for every residential assignment.

A tract house in Lehigh Acres is not the same assignment as a waterfront estate in Naples.

A condominium overlooking the Gulf is not the same assignment as a rural property with subdivision potential.

An older home that has never been listed publicly and has not been updated in fifty years presents different valuation questions than a recently renovated home in a subdivision where twenty nearly identical sales closed during the past six months.

Experienced appraisers know this instinctively.

Consumers generally do not.

They assume every appraisal requires roughly the same amount of work because every appraisal looks roughly the same when it arrives in a PDF.

That could not be further from reality.

Some assignments almost complete themselves because the market provides abundant evidence. Others require hours of additional research, verification with market participants, paired analysis, expanded search parameters, and judgment developed through years of studying how buyers actually behave.

Yet too many assignment systems treat those two jobs almost identically.

The fee may barely change.

The turn time may barely change.

The expectations often do not change at all.

Many appraisers quietly believe the assignment process has become more focused on finding someone willing to perform the work than finding the person best suited to perform it.

That is an important distinction.

If five experienced appraisers decline an assignment because the fee does not reflect the complexity or the deadline is unrealistic, the assignment rarely disappears. It simply continues circulating until someone accepts it.

Maybe that person is highly qualified.

Maybe they are not.

The consumer will never know the difference because they never see that part of the process.

They see an appraiser arrive at the property and naturally assume the system worked exactly as intended.

Sometimes it did.

Sometimes it simply found someone willing to say yes.

Review culture made reports longer, not always better

Review culture creates another layer of frustration.

Appraisers joke that some reviewers spend more time searching for missing checkboxes than reading the report itself.

There is more truth in that joke than many people realize.

Questions routinely come back asking for explanations that already exist three pages earlier in the narrative. Boilerplate commentary grows longer while meaningful analysis remains unchanged. Appraisers spend time rewriting paragraphs that were already correct because someone reviewing the file never actually read them in the first place.

That does not improve valuation quality.

It improves paperwork.

To be fair, thoughtful review work absolutely has value. Every appraiser makes mistakes. Typos happen. Data entry errors happen. Fresh eyes can identify issues that deserve correction before a loan closes.

Nobody should object to that.

What becomes frustrating is when review turns into process management instead of valuation analysis.

Completing a checklist can be taught quickly.

Understanding why buyers pay dramatically different prices for two properties that appear nearly identical on paper takes years of watching transactions unfold in the real world.

That difference matters.

The situation becomes even more complicated when reviewers are not local to the market being appraised. A reviewer sitting hundreds of miles away may have never visited the neighborhood, never seen the competing properties, and never spoken with buyers active in that market. Local knowledge is difficult to replace, particularly in markets where location, views, water access, redevelopment potential, or neighborhood reputation drive value in ways that are not immediately obvious from a spreadsheet.

When the coordinator becomes the producer

Another issue receiving surprisingly little public attention is the growing use of staff appraisers inside some AMC organizations.

Originally, AMCs existed to coordinate assignments and create separation between loan production staff and appraisers.

Many now function as appraisal companies themselves.

They receive assignments, retain part of the appraisal fee, distribute work to independent contractors, and in some markets eventually hire staff appraisers to perform much of that same work internally.

At that point the company is no longer simply coordinating the process.

It is participating in it.

Independent appraisers matter because they create competition, independent judgment, and market diversity. A profession dominated by large organizations controlling assignment flow while simultaneously producing reports should make everyone stop and think about where the industry is headed over the next decade.

Recording information is not the same as understanding it

The same conversation is beginning to develop around hybrid appraisal products and property data collectors.

Supporters argue that collecting property information and analyzing property information are separate jobs.

Conceptually that sounds reasonable.

Reality is messier.

A property data collector can document that a kitchen was renovated.

A competent appraiser understands whether buyers in that neighborhood actually pay more for that renovation, whether the workmanship matches competing properties, whether the renovation changes marketability, and whether it materially affects value compared with recent sales.

Those are not the same job.

Recording information is one skill.

Understanding market reaction is another.

The distinction becomes even more important as valuation models rely increasingly on collected data instead of direct observation by experienced appraisers.

The cheapest part of a million-dollar mistake

The appraisal is the cheapest part of a million-dollar mistake, yet the industry keeps looking for ways to make it cheaper instead of making it better.

That sentence may sound dramatic until you stop and think about the economics.

The appraisal fee represents a tiny fraction of the purchase price, the mortgage amount, the commissions, the lender's exposure, and the buyer's long-term financial commitment. Yet it remains one of the first places many systems look when trying to reduce costs.

Ironically, most borrowers would probably never object to paying another one or two hundred dollars if they knew it meant the lender hired the best-qualified appraiser available for a unique property instead of simply finding the first person willing to accept the assignment. Consumers spend more negotiating a refrigerator allowance than they do questioning how the collateral behind a six-hundred-thousand-dollar mortgage was actually analyzed.

Buyers and sellers see an appraisal fee on a closing statement.

They never see the assignment broadcasts.

They never see the negotiations over fee and turn time.

They never see experienced appraisers declining work because they know the assignment cannot be completed properly under the proposed conditions.

They never see an order bounce across multiple panels before someone finally accepts it.

They simply assume the appraiser who arrived at the property was selected because that person was the best fit for the assignment.

Maybe that assumption is right.

Maybe it is not.

One of the biggest misconceptions in residential lending is that appraisal quality begins when the inspection starts.

It does not.

Quality begins when someone decides who should perform the assignment.

Everything that follows depends on that decision.

The comparable sales selected, the recognition of highest and best use issues, the understanding of buyer behavior, the amount of research performed, and the ability to explain a complicated valuation problem all begin with assigning the right person to the job.

After two decades in this profession, what concerns me most is not that mistakes happen. Every profession makes mistakes.

What concerns me is that quality often feels secondary to workflow because workflow produces measurable statistics while competency does not.

There are lenders that genuinely care about appraisal quality.

There are reviewers who make reports better.

There are certainly AMCs that make a sincere effort to prioritize competency and quality.

There are also systems that reward speed over judgment because speed is easy to measure and judgment is not.

The uncomfortable question is whether the public assumption that the best appraiser was selected for the assignment is always justified.

Buyers and sellers live with the consequences when the valuation supporting one of the largest financial transactions of their lives is treated like another commodity moving through a pipeline.

Part Four moves away from diagnosing problems and asks a different question.

If competency mattered more than workflow, what would a modern appraisal profession actually look like?

Sources and Further Reading

- Cindy Chance, How Regulation and Calcified Appraisal Education Failed Banks, Consumers, and Real Property Valuation, LinkedIn, February 17, 2026: Read the article

- Dodd-Frank Wall Street Reform and Consumer Protection Act: Congress.gov

- Financial Institutions Reform, Recovery, and Enforcement Act of 1989, commonly known as FIRREA: Congress.gov

- CFPB Regulation Z, Section 1026.42, Valuation Independence: Consumer Financial Protection Bureau

- The Appraisal Foundation, USPAP information: The Appraisal Foundation

About the Author

Shane A. White, SRA, AI-RRS, is a Florida Certified Residential Appraiser and owner of Gulf Stream Residential Appraisal LLC, serving Naples, Bonita Springs, Estero, Fort Myers, Marco Island, and surrounding Southwest Florida markets.

If you enjoy thoughtful discussions about residential valuation, appraisal reform, and real estate market analysis, the remaining parts of this series will continue exploring where the profession is headed and why it matters to consumers.

If you need an independent residential appraisal for estate, litigation, divorce, private lending, tax, or complex residential property matters, additional information is available at GulfStreamRes.com.

Hey, I’m Shane. I’m a certified residential appraiser here in Southwest Florida, and I focus on complex valuation assignments and helping people understand real estate value with clarity.